سرویس خبر : فلزات غیرآهنی

ایرالکو بیشترین سهم بازار آلومینیوم بورس کالا را در اختیار دارد

می متالز - شرکتهای ایرالکو و المهدی- هرمزال، 2 عرضهکننده اصلی شمشهای آلومینیومی در بورس کالا محسوب میشوند.

به گزارش می متالز، در حالی که ظرفیت این 2 شرکت تقریبا نزدیک به هم است، سهم قابل توجهی از بازار بورس کالا در اختیار شرکت ایرالکو قرار دارد. علت اصلی این امر را میتوان تقاضای بیشتر بازار برای شمشهایی با خلوص بیشتر دانست. البته داشتن سبد محصولی متنوع نیز در کسب سهم بیشتر بازار کمک شایانی میکند.

مهمترین محصولات در صنعت آلومینیوم را شمشهای آلومینیومی تشکیل میدهند. بازار بورس کالای ایران (IME) همواره کوشیده تا تمامی معاملات محصولات اصلی هر صنعت (از جمله شمشهای آلومینیومی در صنعت آلومینیوم) را جذب کرده و با سازماندهی فرآیندهای داد و ستد، نهتنها از شکلگیری قیمتهای کاذب و بازار سیاه جلوگیری کند بلکه مسیر تأمین نیازهای لازم صنایع پاییندست که از مهمترین فاکتورهای اقتصاد هر جامعهای محسوب میشود را فراهم آورد. در حال حاضر، از بین تولیدکنندگان بالادستی آلومینیوم کشور، تمامی شرکتها از جمله شرکت آلومینیوم ایران (ایرالکو) و المهدی- هرمزال در این بازار فعالیت میکنند و هر ساله بخش قابل توجهی از محصولات خود را به فروش میرسانند. گرچه علاوه بر این 2 شرکت، شرکتهای دیگری چون آلیاژ و ریختهگری فنآوری ذوب گلپایگان و صنایع نگین گلپایگان بهطور پراکنده به عرضه شمشهای آلیاژی آلومینیوم در بورس کالا پرداختهاند، اما دو شرکت ایرالکو و المهدی- هرمزال را میتوان اصلیترین عرضهکنندگان محصولات آلومینیومی در بورس کالای ایران دانست، ضمن اینکه ظرفیت تولیدی این دو شرکت در سطح نزدیکی به هم قرار دارد. در این میان، شرکت ایرالکو با عرضه انواع مختلفی از شمشهای بیلت با آلیاژهای متفاوت، شمشهای خالص (با درجه خلوص متفاوت) و همچنین شمشهای ریختگی آلیاژی مختلف، متننوعترین سبد محصولی در بورس کالا را بهخود اختصاص داده است؛ در حالی که شرکت المهدی- هرمزال تنها شمشهای خالص با درجه خلوص 99.5، 99.7 و 99.75 درصد در بورس کالا عرضه کرده است.

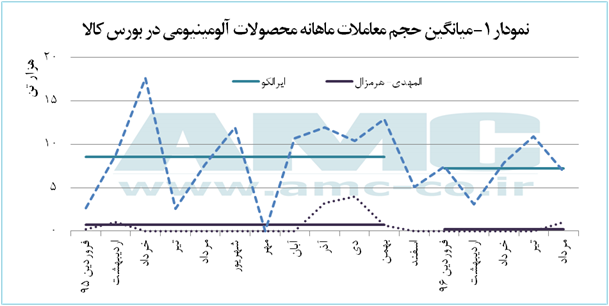

نمودار 1، میزان حجم معاملات ماهانه انواع محصولات آلومینیومی عرضه شده در بورس کالای ایران را از ابتدای سال گذشته تا پایان ماه پنجم سال جاری (مرداد) نشان میدهد. همانطور که در این نمودار قابل مشاهده است، میزان معاملات شرکت ایرالکو در قیاس با حجم معاملات المهدی- هرمزال در سطح بسیار بالاتری قرار دارد. در طول دوره مورد بررسی تنها یک ماه شرکت ایرالکو در بورس کالا حضور نداشت و بدین ترتیب معاملهای را به ثبت نرساند؛ در حالی که در مورد المهدی- هرمزال 4 ماه شامل مرداد و مهر سال 1395 و همچنین خرداد و تیر سال جاری در بورس کالا عرضهای نداشت و در ماههای دیگر با وجود عرضه شمش آلومینیومی، موفق نشد معاملهای را صورت دهد. این حجم معاملات صفر در ماههای مختلف برای شرکت المهدی- هرمزال در سال گذشته سبب شد تا میانگین معامله ماهانه ایرالکو در سال گذشته حدود 11.2 برابر شرکت المهدی- هرمزال باشد. در همین حال، عدم حضور پر رنگ المهدی- هرمزال در سال جاری سبب شد تا این اختلاف باز بیشتر شده بهگونهای که میانگین معاملات ماهانه شرکت ایرالکو در سال جاری 36.2 برابر حجم معاملات المهدی- هرمزال شود.

عدم وجود تقاضا، تنها علت صورت نگرفتن معامله در تمامی ماههای بدون فروش برای شرکت المهدی- هرمزال در بورس کالا بود. همانطور که پیشتر نیز اشاره شد این شرکت تنها به عرضه شمشهای خالص با خلوص کمتر از 99.75 درصد میپردازد در حالیکه رقیب آن یعنی شرکت ایرالکو محصول مشابهی با درجه خلوص حداقل 99.8 درصد را عمدتا روانه این بازار میکند. از این رو، بهنظر میرسد که تقاضای بیشتری برای شمشهای آلومینیومی با درجه خلوص بالاتر در بازار وجود داشته باشد.

منبع: اخبار فلزات

عناوین برگزیده

دو دقیقه پیش

دو ساعت پیش

هفت ساعت پیش

بیست و دو ساعت پیش

یک روز پیش

دو روز پیش

دو روز پیش

مدیرعامل شرکت سرمایهگذاری توسعه معادن و فلزات عنوان کرد:

افتتاح نخستین طرح پیشران اقتصادی با سرمایهگذاری "ومعادن"/ سرمایهگذاری ۳.۵ میلیارد دلاری "ومعادن"

اطلاعیه فرابورس برای واگذاری استقلال و پرسپولیس

افتتاح بزرگترین کارخانه فروسیلیس ایران در دامغان طی سفر دولت سیزدهم

قیمت جهانی طلا امروز ۱۴۰۳/۰۱/۲۹

در مجمع عمومی عادی سالیانه صبا فولاد؛

«فصبا» ۷۰ تومان سود تقسیم کرد

بازار طلای جهانی اندکی سرد شد

درج شرکت آلیاژ گستر هامون در بازار دوم فرابورس ایران

صبا فولاد خلیج فارس «فصبا» ۷۰ تومان سود تقسیم کرد/ پروژه احیای مستقیم «فصبا» سال ۱۴۰۵ به بهرهبرداری میرسد

تغییرات مدیریتی با تمرکز بر اهداف فنی و توسعهای/ فسادستیزی اساس کار در ایمیدرو است

یورو رکورد زد

طلای جهانی از تکاپو افتاد

قیمت نفت با کاهش ذخایر آمریکا صعودی شد

اقتصاد فوتبال ایران رونق میگیرد؟

بانکهای چینی در معرض تحریم

بیتکوین آماده شد

تبلور افتخار، اقتدار و ایستادگی؛

ابرطرح زمزم سه در نیمه بهار به ظرفیت نامی رسید

فناوری داغ معدن در سال ۲۰۲۴/ نرمافزار، حسگرها، اتوماسیون و اکتشاف در صدر فهرست قرار دارند

مساله ساعت کار کارگری

تورم نقطهای در کف ۳.۵ سال

وزیر صمت: شورای رقابت مسوول قیمت پژوپارس است

جزئیات پیشرفت پروژه عظیم مجتمع مس جانجا اعلام شد

افتتاح نخستین طرح پیشران اقتصادی کشور با سرمایهگذاری «ومعادن»

ضرورت جذب سرمایهگذاری مالی و مشارکت مردمی برای توسعه معادن

افتتاح بزرگترین کارخانه فروسیلیس ایران در دامغان طی سفر دولت سیزدهم

ثبت بالاترین میزان تاریخ تولید فولاد ایران در سال ۱۴۰۲

یورو رکورد زد

طلای جهانی از تکاپو افتاد

قیمت نفت با کاهش ذخایر آمریکا صعودی شد